Investment Planning

Your investment plan provides the framework for your investment decisions. It ensures that the decision-making process with respect to the management of your portfolio will be consistent, even when unexpected market fluctuations tempt distraction from your long-term strategy.

Specific investment recommendations should always be made in concert with the guidelines that we agree upon and will outline in your investment plan.

A number of factors need to be considered when developing an investment plan;

- Goal; what will the money be used for and when do you need it?

- Risk tolerance; what levels of volatility can you accept?

- Investment vehicle; what is the most appropriate investment vehicle given your circumstances; such as TFSA, RRSP, RESP, Pension, Non-registered acct.?

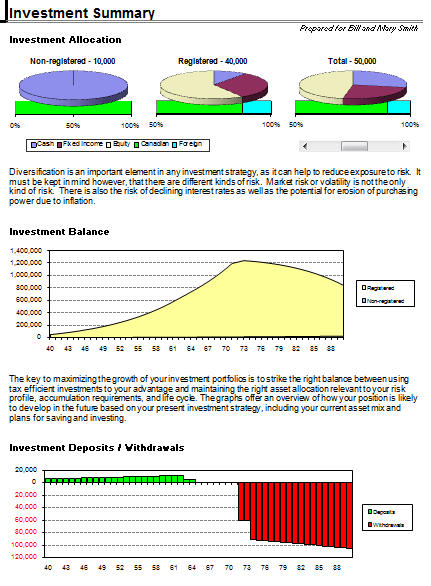

- Asset allocation: fixed income, stocks, real estate, other investments

- Projected Rate of Return: given your asset allocation what rate of return can you expect? What rate of return do you require to achieve your goal?

- Monitoring Schedule: how often will you review your investments and make necessary adjustments?